Graphical exploratory data analysis

Histogram

# Import plotting modules

import matplotlib.pyplot as plt

import seaborn as sns

# Set default Seaborn style

sns.set()

# Compute number of data points: n_data

n_data = len(versicolor_petal_length)

# Number of bins is the square root of number of data points: n_bins

n_bins = np.sqrt(n_data)

# Convert number of bins to integer: n_bins

n_bins = int(n_bins)

# Plot histogram of versicolor petal lengths

_ = plt.hist(versicolor_petal_length, bins = n_bins)

# Label axes

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('count')

# Show histogram

plt.show()

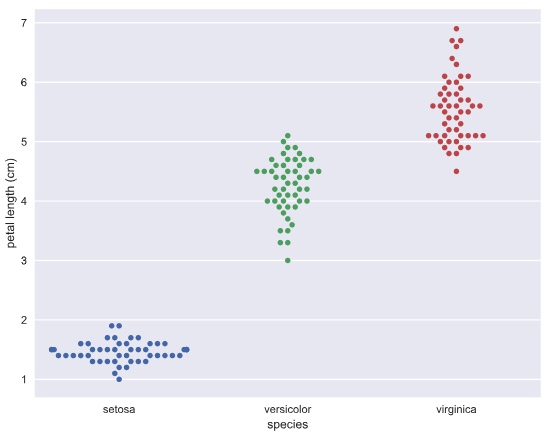

Bee swarm plot

# Create bee swarm plot with Seaborn's default settings

_ = sns.swarmplot(x='species', y = 'petal length (cm)', data = df)

# Label the axes

_ = plt.xlabel('species')

_ = plt.ylabel('petal length (cm)')

# Show the plot

plt.show()

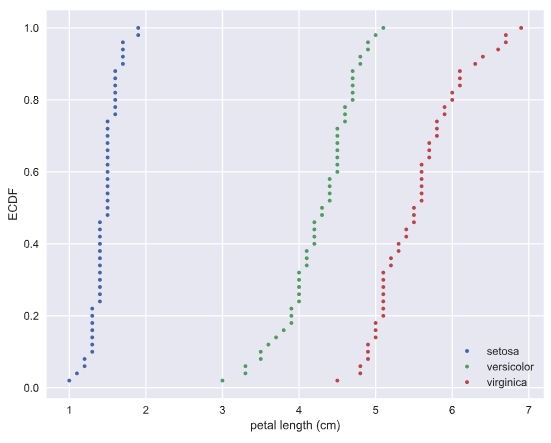

Empirical cumulative distribution functions

CDF gives the probability the measure of the speed of light will be less than the value of x axis.

def ecdf(data):

"""Compute ECDF for a one-dimensional array of measurements."""

# Number of data points: n

n = len(data)

# x-data for the ECDF: x

x = np.sort(data)

# y-data for the ECDF: y

y = np.arange(1, (n+1)) / n

return x, y

# Compute ECDFs

x_set, y_set = ecdf(setosa_petal_length)

x_vers, y_vers = ecdf(versicolor_petal_length)

x_virg, y_virg = ecdf(virginica_petal_length)

# Plot all ECDFs on the same plot

_ = plt.plot(x_set, y_set, marker='.', linestyle='none')

_ = plt.plot(x_vers, y_vers, marker='.', linestyle='none')

_ = plt.plot(x_virg, y_virg, marker='.', linestyle='none')

# Annotate the plot

plt.legend(('setosa', 'versicolor', 'virginica'), loc='lower right')

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('ECDF')

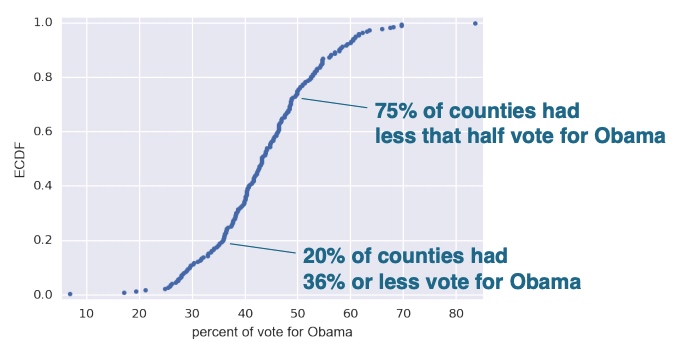

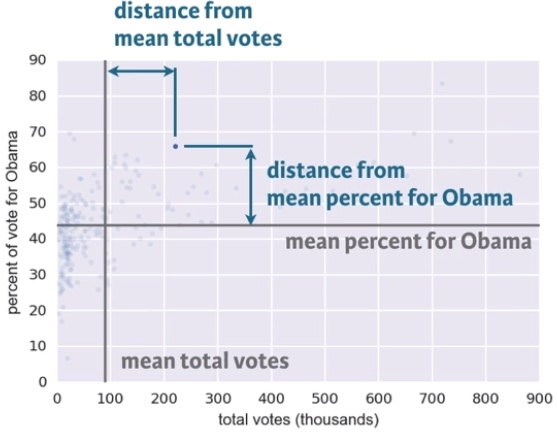

Another example: the dataset contains the percentage of vote for Obama for each county.

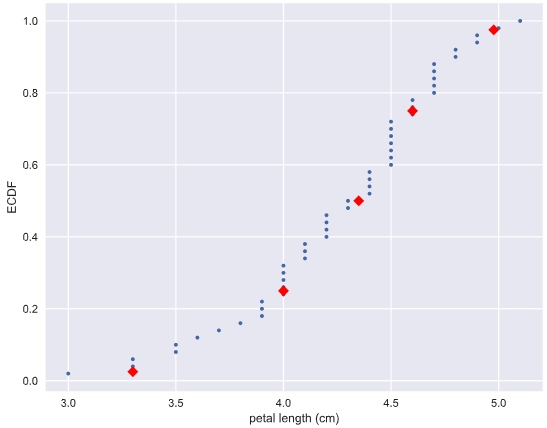

Plot percentile on ECDF

# Specify array of percentiles: percentiles

percentiles = np.array([2.5, 25, 50, 75, 97.5])

# Compute percentiles: ptiles_vers

ptiles_vers = np.percentile(versicolor_petal_length, percentiles)

# Plot the ECDF

_ = plt.plot(x_vers, y_vers, '.')

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('ECDF')

# Overlay percentiles as red diamonds.

_ = plt.plot(ptiles_vers, percentiles/100, marker='D', color='red',

linestyle='none')

# Show the plot

plt.show()

Quantitative exploratory data analysis

Covariance and Correlation

# Make a scatter plot

_ = plt.plot(versicolor_petal_length, versicolor_petal_width, marker='.', linestyle='none')

# Label the axes

_ = plt.xlabel('versicolor petal length (cm)')

_ = plt.ylabel('versicolor petal width (cm)')

# Show the result

plt.show()

Pearson correlation coefficient: It is a comparison of the variability in the data due to codependence(the covariance) to the variability inherent to each variable independently (their standard deviations).

def pearson_r(x, y):

"""Compute Pearson correlation coefficient between two arrays."""

# Compute correlation matrix: corr_mat

corr_mat = np.corrcoef(x, y)

# Return entry [0,1]

return corr_mat[0,1]

Discrete variables

Given a set of data, you describe probabilistically what you might expect if you collect the same data again and again and again.

Bernoulli trial and binomial distribution

def perform_bernoulli_trials(n, p):

"""Perform n Bernoulli trials with success probability p

and return number of successes."""

# Initialize number of successes: n_success

n_success = 0

# Perform trials

for i in range(n):

# Choose random number between zero and one: random_number

random_number = np.random.random()

# If less than p, it's a success so add one to n_success

if random_number < p:

n_success += 1

return n_success

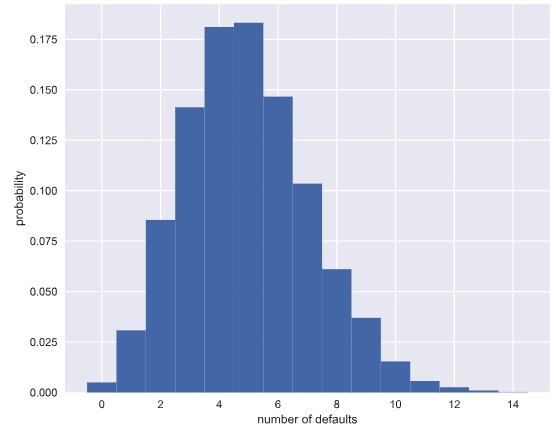

Try 1,000 times of 100 Bernoulli trial and save the number of loan defaults in to a list

# Initialize the number of defaults: n_defaults

n_defaults = [None] * 1000

# Compute the number of defaults

for i in range(1000):

n_defaults[i] = perform_bernoulli_trials(100, 0.05)

Compute the probability of n_default >= 10

# Compute the number of 100-loan simulations with 10 or more defaults: n_lose_money

n_lose_money = np.sum(n_defaults >= 10)

# Compute and print probability of losing money

print('Probability of losing money =', n_lose_money / len(n_defaults))

Output: Probability of losing money = 0.022

Probability mass function (PMF): The set of probabilities of discrete outcomes

Distribution: a mathematical description of outcomes

Binomial distribution: The number of r of successes in n Bernoulli trials with probability p of success, is Binomially distributed.

E.g. The number r of heads in 4 coin flips with probability 0.5 of heads, is Binomially distributed.

# Conduct the 4 coin flips for 1000 times

samples = np.random.binomial(4, 0.5, size = 1000)

Plot the Binomial PMF

Plot the PMF of the Binomial distribution as a histogram. The trick is setting up the edges of the bins to pass to plt.hist() via the bins keyword argument. We want the bins centered on the integers. So, the edges of the bins should be -0.5, 0.5, 1.5, 2.5, ...up to max(n_defaults) + 1.5

# Compute bin edges: bins

bins = np.arange(0, max(n_defaults) + 2) - 0.5

# Generate histogram

_ = plt.hist(n_defaults, bins = bins, normed=True)

# Label axes

_ = plt.xlabel("number of defaults")

_ = plt.ylabel("probability")

# Show the plot

plt.show()

Poisson distribution

Poisson event: the time of the next event is completely independent of when the previous event happened.

The parameter for poisson distribution: the average number of arrivals in a given length of time

Story: The number r of hits on a website in one hour with an average hit rage of 6 hits per hour is Poisson distributed.

Relationship between Binomial and Poisson distribution

Say we do a Bernoulli trial every minute for an hour, each with a success probability of 0.1. We would do 60 trials, and the number of successes is Binomially distributed, and we would expect to get about 6 successes. This is just like the Poisson story we discussed in the video, where we get on average 6 hits on a website per hour. So, the Poisson distribution with arrival rate equal to np approximates a Binomial distribution for n Bernoulli trials with probability p of success (with n large and p small). Importantly, the Poisson distribution is often simpler to work with because it has only one parameter instead of two for the Binomial distribution.

Continuous Variables

Probability density function (PDF)

PDF is mathematical description of the relative likelihood of observing a value of a continuous variable Area under the PDF gives probabilities

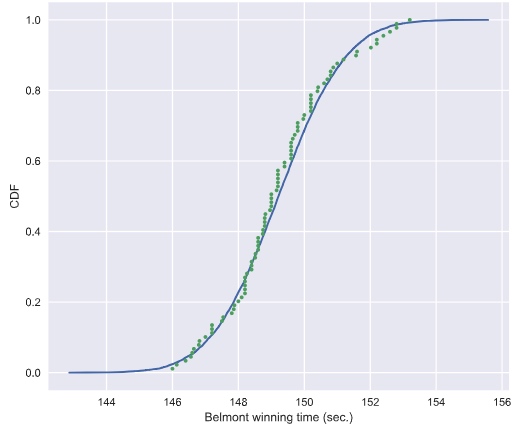

Test if a dataset is normally distributed

# Compute mean and standard deviation: mu, sigma

mu = np.mean(belmont_no_outliers)

sigma = np.std(belmont_no_outliers)

# Sample out of a normal distribution with this mu and sigma: samples

samples = np.random.normal(mu, sigma, size = 10000)

# Get the CDF of the samples and of the data

x_theor, y_theor = ecdf(samples)

x, y = ecdf(belmont_no_outliers)

# Plot the CDFs and show the plot

_ = plt.plot(x_theor, y_theor)

_ = plt.plot(x, y, marker='.', linestyle='none')

_ = plt.xlabel('Belmont winning time (sec.)')

_ = plt.ylabel('CDF')

plt.show()

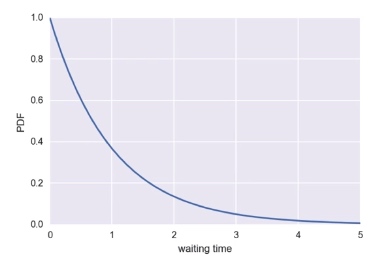

Exponential Distribution

The waiting time between arrivals of a Poisson process is Exponentially distributed. It has a single parameter, the mean waiting time.

Source

https://www.datacamp.com/courses/statistical-thinking-in-python-part-1